Innovation

Analysis

Added Value, a famous unknown

September 2, 2020

Facebook is one of the largest communication platforms but doesn’t generate its own content; it boasts some 2.2 billion users. The World Health Organisation uses TikTok to report on the COVID-19 by finding new ways to transmit messages to other stakeholders. Uber has no vehicles of its own however it has overtaken other taxi companies. Clearly, the rules of the game have changed and the concept of how we explain what a company represents has also changed. The focus now is on how a company transforms the revenue it receives, that is to say, how it creates value.

Highlights

- Reporting on “added value” with “Integrated Reporting- IR” is becoming a more relevant matter for organisations/ companies in the private and public sector alike.

- Although Integrated Reporting was initially conceived with the private sector in mind, it brings many benefits for public sector organisations as well.

- The public sector has a major impact on the environment and uses a great deal of resources. IR’s emphasis on mid- and long-term value creation encourages integrated thinking, which supports better decision making, greater transparency and more sustainable, public governance, policies and services.

Reporting on “added value” is becoming more relevant for organisations in the private and public sector. The International Integrated Reporting Council (IIRC) defines integrated reporting as: ‘a process founded on integrated thinking that results in a periodic integrated report by an organisation about value creation over time and related communications regarding aspects of value creation’. Companies inform through published non-financial information to their stakeholders and in the public sector with communication aimed at citizens.

How do companies actually add value?

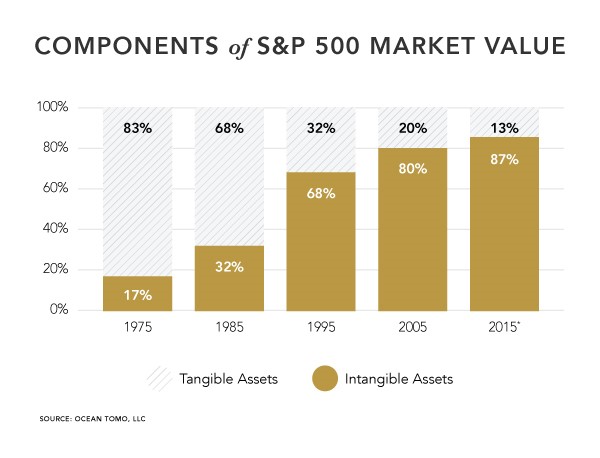

According to the Ocean Tomo study, in 1975, 83% of a company’s value was explained using financial values, however, other factors have become more significant over time. In 2015, 87% of a company’s value comprised intangible assets, with financial assets shrinking to 13% .

What is the current situation in the public sector?

Defining and measuring value creation in the public sector is more complicated. The Work Foundation, in its publication “Deliberative democracy and the role of public managers” begins by outlinung: “Public value is what the public values. Managers in public services must find out what people want through the democratic processes of deliberation and public engagement, in order to make a better connection between the preferences of citizens and the services they provide.”[1] It is possible that the non-financial information and integrated report can make the added value of the public sector more visible.

How can added value be transmitted through integrated reporting?

Non-financial information and the Integrated Report have made very important progress in recent years, particularly in the European Union, due to EU Directive 2014/95, which member countries have transposed into their own regional legislation. For this reason, large companies in the EU have been required to disclose more information in their annual reports, such as their policies and associated risks in relation to environmental protection, social responsibility, treatment of employees, respect for human rights, anti-corruption and bribery and diversity on company boards.

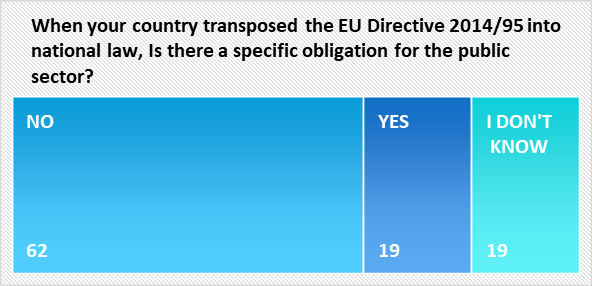

According to a survey carried out by the ECIIA (European Confederation of Institutes of Internal Auditing) and EUROSAI (European Organisation of Supreme Audit Institutions), in a common project regarding this topic, only 19% of European countries that transposed the EU Directive 2014/95 into national law included specific obligations for the public sector, which is why the Public Sector is clearly in the tailwind of the Private Sector.

In its beginning, the Integrated Reporting framework, IIRC, highlights that “It is written primarily in the context of private sector, for-profit companies of any size but it can also be applied, adapted as necessary, by public sector and not-for-profit organisations”. The Public Sector should set an example when conveying non-financial information to its stakeholders; it should explain how it creates value and will continue to do so in the mid-and long-term.

Case study

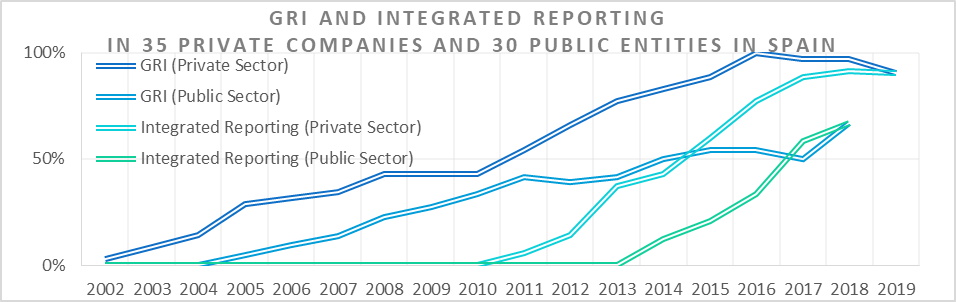

Taking Spain as an example: an analysis was carried out into how 35 large private companies and 30 public entities were reporting on economic, environmental and social performance and how they use the Global Reporting[2] framework in public information and the Integrated Reporting. Initiative guidelines on sustainability and integrated reporting showed that implementation in the public sector was at least four years behind.

What is the current role for internal and external auditors in the public sector?

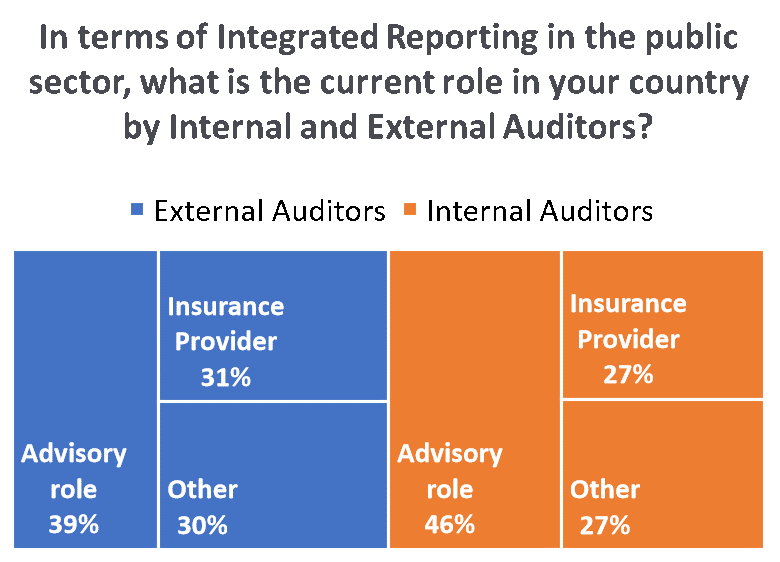

In the recent ECIIA and EUROSAI survey, 20 European countries answered questions about the role of external and internal auditors in the Integrated Report in the public sector.

In 39% of the countries, external auditors provide advice to public sector organisations on integrated reporting and 31% have an assurance role. Regarding the internal auditors, 46% have an advisory role but only 27% work as the assurance provider. The response “other” representing 30%, is due to the fact that internal and external auditors don’t participate in these activities.

These results indicate that there is still much to develop and auditors, both internal and external, contribute to integrated reporting initially in an advisory role, changing to an assurance role when it is implemented.

Conclusions

The public sector should set an example when conveying non-financial information to its stakeholders. Faced with limited budgets, a changing environment and ever increasing demands from citizens for more transparency in the management and use of resources and it must explain how it creates value and how it will continue to do so in both the mid and longer term.

The public sector must “rise” to this challenge and play a leading role in Integrated Reporting. Both internal and external audit must help in this process.

[1] HORNER, L. LEKHI, R. BLAUG, R. Deliberate democracy and the role of public managers. Final Report of The Work Foundation’s public value consortium. The Work Fundation. 2006. (www.theworkfoundation.com)

[2] GRI, Global Reporting Initiative is a global standard of guidelines for the preparation of sustainability reports for those companies who wish to evaluate their economic, environmental and social performance.

About the expert Soledad Llamas Tutor is Director of Internal Audit, Risk Management and Internal Control at Canal de Isabel II Soledad Llamas is an MSc Civil Engineer, MBA, CIA, CCSA, CRMA and the first certified COSO in Spain. She is responsible for the implementation of the internal audit and risk management program in Canal de Isabel II, the public company which provides all the water services for the Community of Madrid, Spain. Since 2013 Soledad has collaborated with ECIIA (European Confederation of Institutes of Internal Auditing) and EUROSAI (European Organisation of Supreme Audit Institutions) to establish common auditing guidelines for Internal Audits in Public Entities and SAI’S, and since 2017 she has been the Chair of the working group of both organisations. She has published articles in journals such as “Revista de Control Externo de España”, Spain’s SAI, regarding “Non-financial reporting in the Public Sector” and “Revista de Auditoría Interna”, Institute of Internal Audit of Spain, regarding “COSO, Internal Control in the Public Sector”. Soledad is a regular speaker at conferences and courses of the Ministry of Finance, the Supreme Audit Institute of Spain and International Congress of Internal Audit. |

The views in this article are the author’s only, and do not necessarily represent the views of the OECD or its member countries.

Let’s Discuss

Innovation

- You must be logged in to reply to this topic.